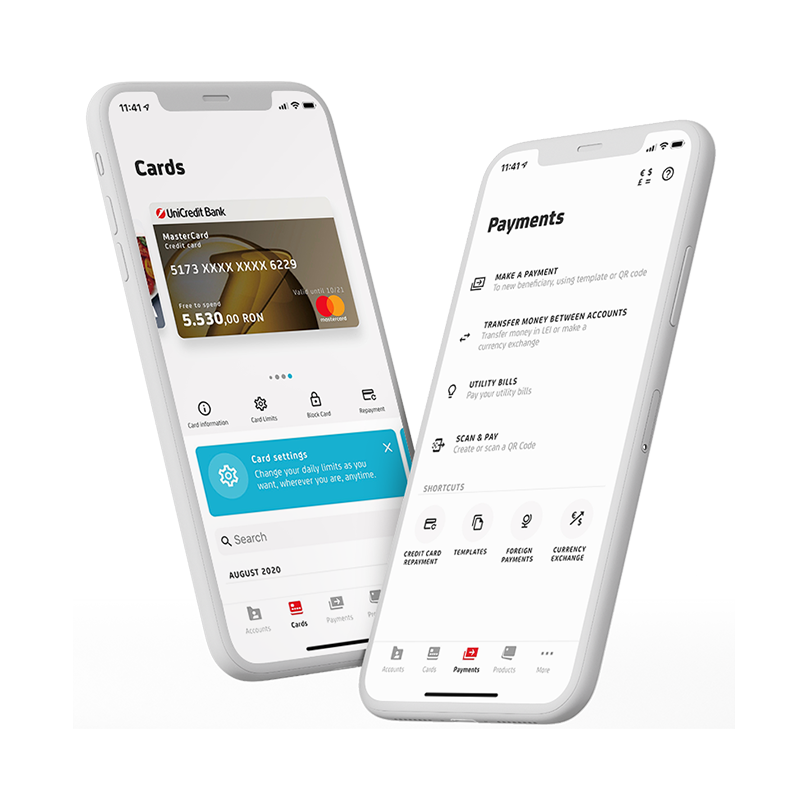

Activate now Mobile Banking with ZERO administration fees I WANT THE APP Google Play button App Store button Huawei Store button